.png)

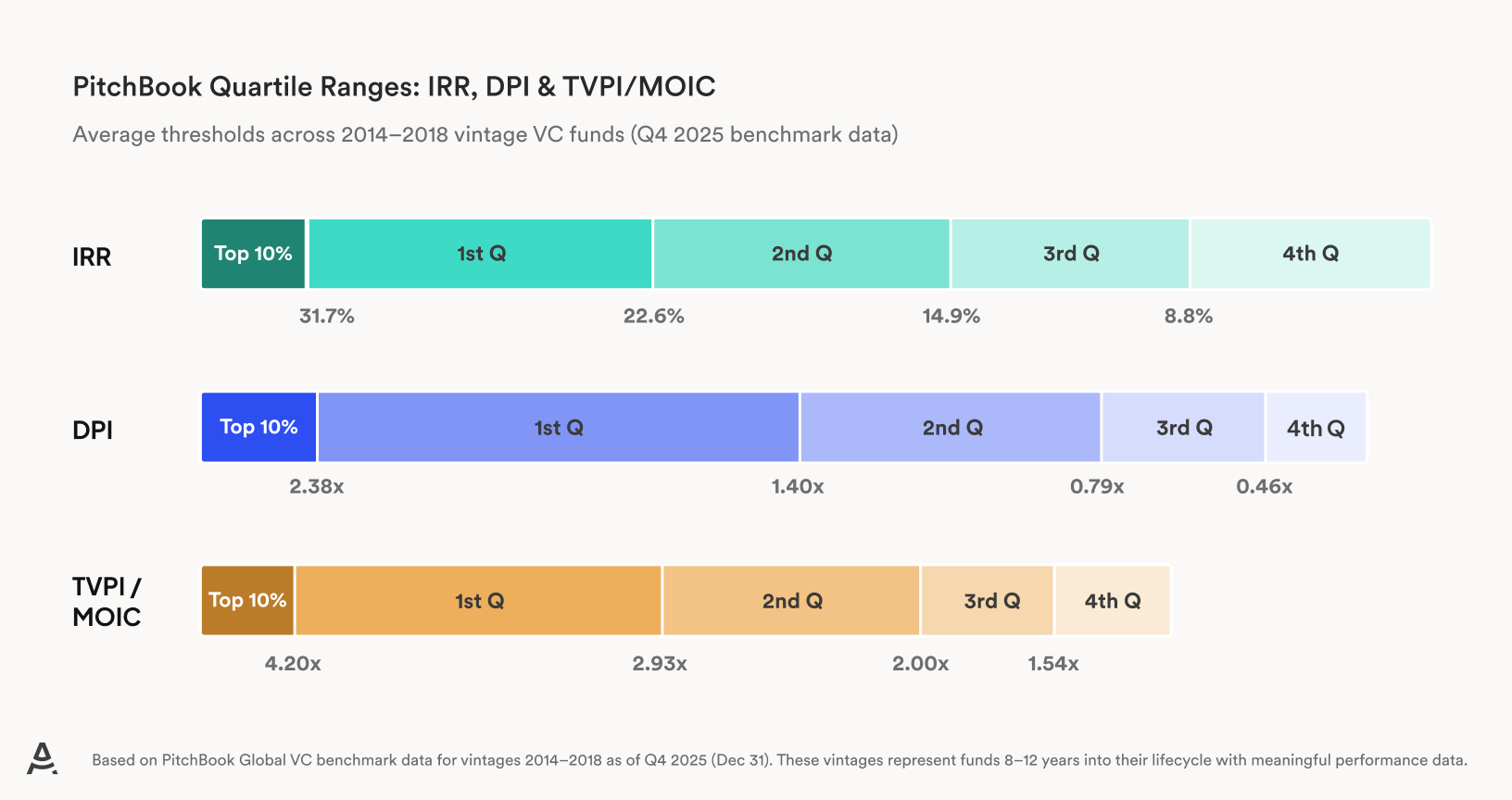

Venture capital is rarely more in focus than it is today, driven by AI's potential to reshape industries and a pipeline of highly anticipated IPOs carrying valuations in the hundreds of billions and in some cases trillions. While we share the enthusiasm, perspective matters. These outcomes took many years to build, and for every success there are countless companies that fell short. Private markets are often praised for their headline returns, but the range of outcomes is wide, which is why access and selectivity tend to matter more here than in other asset classes. Nowhere is this more apparent than in venture, as the chart below illustrates.

The data above shows the most recent cohort of mature venture vintages, those between 7 and 11 years old, and their performance across the three most commonly quoted metrics: how much capital has been returned (DPI), total multiple of dollars invested (TVPI/MOIC), and internal rate of return (IRR). Focusing on IRR, the midpoint sits roughly in line with what a public markets investor would have earned over the same period. If we shift above that midpoint, the picture becomes increasingly compelling, shown by the threshold for the top 25% coming in at 22.6%. That gap between the median and the top quartile underscores the potential impact of manager selection.

The challenge is that venture capital is largely dominated by a mix of established and emerging managers who are highly coveted, well-networked, and rarely in need of new investment partners. Together, these dynamics turn access into a binding constraint, not a nicety. Without it, the outcomes that justify locking up capital for a decade may be less likely.

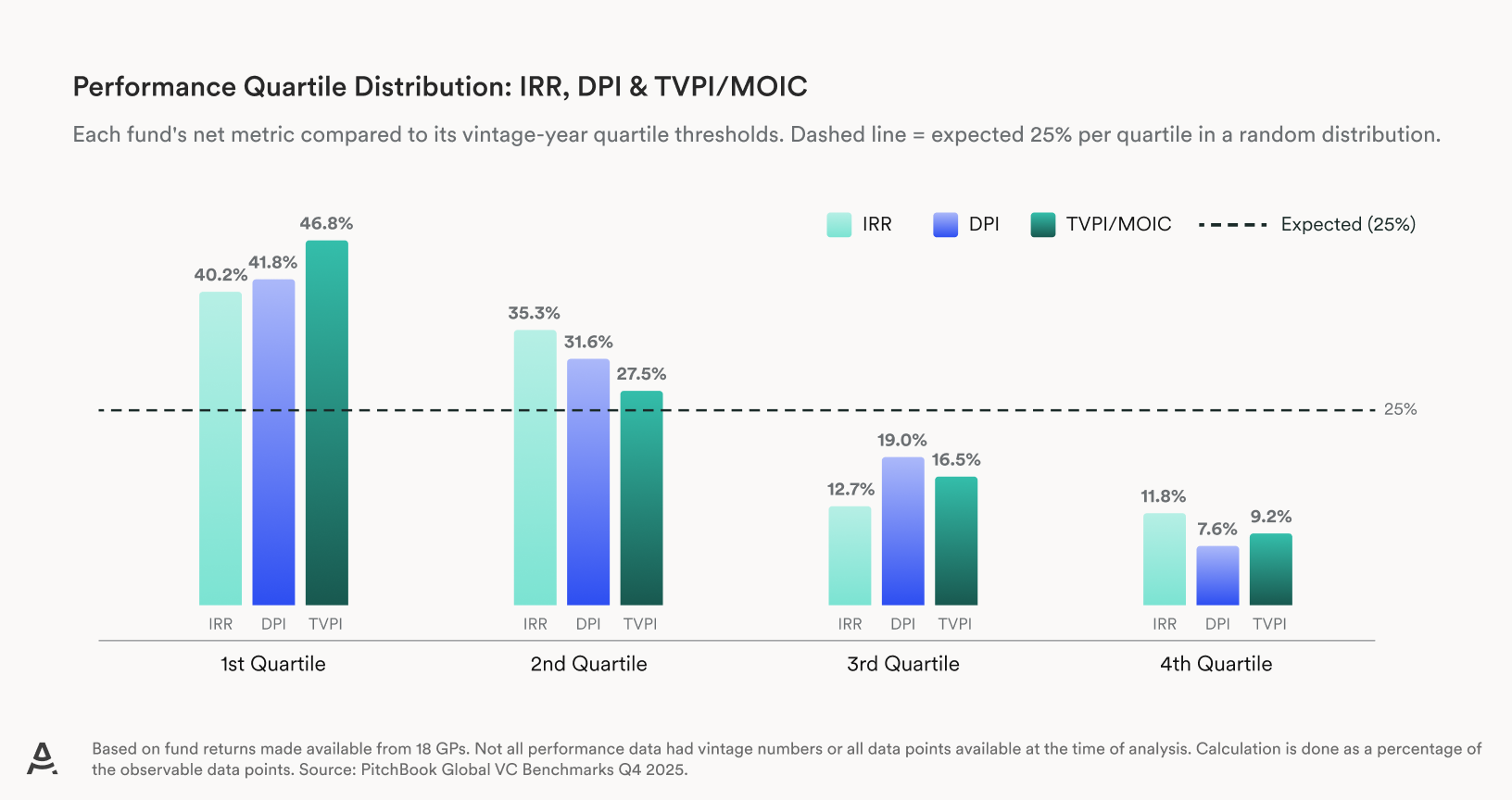

At Allocate, we seek to build relationships across a range of managers. We attempted to capture this on a backward-looking basis. The visual below offers a small window into that picture – the net performance of the managers our research team has deeply reviewed over the past month. As a benchmark, representation above 25% in each of the top two quartiles is a good indicator of strong historical performance, which by extension may be associated with less exposure to third- and fourth-quartile managers, with the latter being the most important to avoid.

Among the 18 GPs we met with and formally evaluated, the track record data is encouraging. More than 70% of their funds have ranked in the top half, which means these managers have delivered above-median returns nearly three quarters of the time. Even more striking, over 40% have ranked in the top quartile, nearly double the rate of the broader market. Additionally, on the downside, these managers have been twice as effective as the market at avoiding fourth-quartile outcomes. In short, this group has historically excelled at capturing the best opportunities while avoiding the worst.

Does strong access alone guarantee differentiated returns? Not at all. But if even a portion of the performance seen across more than 100 previously analyzed vintages reflects skill, then there is some signal that can potentially be captured. Discerning this difference, while recognizing that market dynamics make outcomes inherently unpredictable, is precisely what our research team is here to assess. We look carefully at each manager to separate what is likely repeatable from what was luck, with the goal of identifying the groups we believe are best positioned, based on our current assessment, to keep delivering differentiated outcomes.

What this analysis looks like and how we assess the probability of good outcomes is something we will cover in detail in the future, but at the highest level, effective manager selection involves seamlessly blending quantitative rigor and qualitative assessment in an iterative process focused on separating signal from noise. The right mix of these two factors shifts from strategy to strategy and in some cases at the sub-strategy level. Refining this balance is a constant work in progress, and for us as research professionals, the pursuit of better decision-making is in itself the reward.

IMPORTANT NOTES

This material is for informational purposes only and does not constitute investment advice or a recommendation. Past performance is not indicative of future results. The analysis referenced is based on a limited sample of managers reviewed over a specific period and may not be representative of broader market outcomes. There can be no assurance that similar results will be achieved.

.png)